A Friendly Conversation with a Banker

Mike: Who are you?

Banker: I’m 28 and am a vice president at a large global bank where I’m currently earning about $250,000 a year. I grew up in the South, went to public school, then a private college. I got an internship on Wall Street, and then a full-time job. That was in 2005, and many rounds of layoffs later, I’m still there.

Mike: What did you study as an undergrad?

Banker: Originally, Asian Studies, but then I added on a business program as well.

Mike: What kind of careers were you considering when you were in college?

Banker: Not many! I always thought I would run my own business. I’m very opinionated, and didn’t think I would last long working for someone else. I didn’t know what kind of business — my dad was (is) an entrepreneur. I figured I would jump on the first good idea that I ran across, fail a couple of times, and then find something that worked. When the Wall Street opportunity came up, I thought it would be a good place to learn some business skills, so I jumped at it. I was right, but I overestimated my ability to quit when I came across a good idea.

Mike: What kind of upbringing did you have? I take it that since your father is an entrepreneur, it wasn’t one where you worried about money or bills?

Banker: Correct, although my dad did run a few businesses into the ground, and he had a nightmare divorce that sucked time and money away until I was 16. Money might have been tight once or twice, but it never felt like it when I was a kid.

Mike: Did your parents talk to you about money while you were growing up?

Banker: Oh, god yes.

Mike: Haha — in what ways?

Banker: I mean, I remember teaching my dad how to look up his stock quotes on Prodigy in the early days of the Internet.

Mike: How old were you then?

Banker: I must have been about seven. My dad would teach me about stocks, compound interest, and investing.

Mike: Wow. At seven years old?

Banker: It was the beginning of the Internet bubble, so that had something to do with it. I think if stocks hadn’t been going straight up at the time, I might not have had the same level of exposure. In any case, when I would work summer jobs I would save it and invest it — even if it was only a couple of hundred dollars.

Mike: What kind of summer jobs did you have?

Banker: Well, my first summer job was sewing buttons onto men’s shirts at my dad’s dry cleaning plant. I worked for $5 per hour or something. It was hot — summer in the Deep South surrounded by steam-powered machines. I also worked in restaurants, and later got unpaid (and then paid) internships at financial services firms. I was also a camp counselor, which was maybe the best job I ever had.

Mike: Sewing buttons and working in restaurants — it sounds like your family wanted you to experience good old fashioned manual labor.

Banker: Exactly. My parents always made sure that I knew not to take anything for granted, which is good, because that helped me avoid a lot of the problems that kids run into when they end up in high-paying jobs right out of college.

Mike: What kinds of problems?

Banker: I think most people get these banking or consulting jobs, and when you start out with a base salary of $60,000 or $70,000 right out of college, you probably have more disposable income than at any other point in your life. It’s a shock. All of a sudden your bank account is filling up (unless you moved into a really expensive studio/one-bedroom apartment). So I know many people, especially in 2006–2007, who were spending everything they made, and some were spending more than they made because they were betting on higher future income.

Mike: What are they spending money on? These are 22 and 23-year-olds we’re talking about?

Banker: Yeah, so, clothes, shoes, jewelry and electronics at first, and when you had the newest everything, then it was restaurants and clubs and trips to Vegas.

Mike: You managed to avoid all of that?

Banker: Of course not. =)

Mike: Haha, what does that mean?

Banker: I mean, it doesn’t matter how responsible your upbringing was, there’s still the peer pressure to live extravagantly when you’re surrounded by it. So I would eat out at nice restaurants, and occasionally I would go to a club, but I was never comfortable with the idea of spending $400 on a bottle of vodka. Mostly, I think what helped the most was that I made a decision at the very beginning that I would live on my base salary. So when there were big bonuses, that all went straight to savings.

A lot of that was reinforced during the financial crisis — there would be senior people complaining about how they couldn’t live on a $250,000 to $400,000 base salary, and I never wanted to be in that position.

Mike: Do you think it’s part of the banking culture to spend a lot of money? I imagine if it were me, I wouldn’t want to spend very much money, but I’d also imagine I’d lose out because of it — networking and such.

Banker: There is some of that, but the vast majority of professional connections (up to a certain level) can either be taken care of with $6 beers at the local bar near the office, or with an expense account. This might just be New York.

Mike: So the big spending you’d say is mostly due to having so much disposable income for the first time, and feeling like there so much more money coming your way, so why not?

Banker: Right, also (and I think that this is something that comes across on the site) a lot of people don’t grow up with strong personal finance skills, regardless of background. Did you see the article in The New York Times about vet school this week? I feel like the best evidence that there is a huge group of people who don’t have enough personal finance skills is all the people in graduate programs who are going to find themselves in financial ruin. The return on investment for so many of the programs is negative, and the worst part is that the debt follows you forever. It’s criminal that student loans are the ONLY mainstream type of debt that can’t be cleared by bankruptcy. That was a roundabout way of making the point that you can’t bet on what your income is going to be in 10 to 20 years.

Mike: Can you walk me through your career trajectory? It’d be great to get some insight into how it all works — I’m sure there’s a clear path that you see, and income levels you expect to hit at certain points.

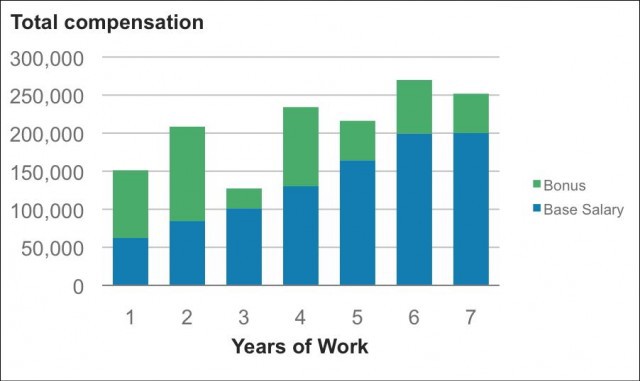

Banker: I’m going to send you a chart.

Mike: Amazing.

Banker: So, I keep a spreadsheet with all of my income, taxes, investment returns, spending.

Mike: You mean, an Excel spreadsheet?

Banker: Yep. Use the tools you know, right? And I use Mint.com to track my spending — that website has changed my life. It’s so great (and they do not pay me to say that!).

Mike: Haha. I track everything in my head. But it works!

Banker: Impressive!

Mike: I also don’t have as much to track as you, so I bet it’s much more helpful.

Banker: The hardest part is keeping track of cash transactions. I lose track of all those and it makes me sad that that data is gone forever.

Mike: Why are the bonuses in years one and two so high?

Banker: Because I was awesome! Just kidding. The first two years were the last two “good years” on Wall Street. The third year is 2009. And in 2010–2011, Wall Street raised everyone’s base salaries to avoid bad “bonus” headlines, which was an incredibly dumb business move. The whole point of having bonuses be a large part of overall compensation is so that you can CUT compensation when times are tough. We learned from Keynesian economics that people get upset if you cut their salaries.

Mike: So, the banks raised salaries to save face?

Banker: Yes. It’s not the first time the industry acted dumb all at the same time.

Mike: What kind of banking do you do?

Banker: I work on the institutional side of an investment bank, in a client-facing role. I’m Dealbreaker’s target audience.

Mike: What’s the end goal for the typical banker?

Banker: Managing Director, or, Partner if you’re at Goldman Sachs. The typical path is: analyst (years 1–3) → associate (years 3–5) → vice president (years 5–7+) and then there are usually one or two more intermediate titles and then you’re finally a Managing Director. I think the youngest MD I’ve known is 31.

Mike: You’re getting there!

Banker: Hah. Yeah, that’s not good! Because if you don’t make MD by your late thirties, you’re usually not going to get it at all.

Mike: But usually that’s because you’re not good at what you do?

Banker: I mean, it’s difficult to make it to MD if you’re not good at what you do. But being good isn’t enough, by any stretch. These are huge bureaucratic institutions with opaque compensation and promotion practices, usually with power concentrated at one or two key individuals. So, in order to get promoted, the most important thing you have to do is not piss off the people above you. I think this is the case in most large organizations, not just banks, and not just for-profit organizations either. Any job with layers of bureaucracy is going to be mostly politics.

Mike: And if you don’t make it to managing director, you’re stuck in purgatory forever?

Banker: Not forever — just until the next round of layoffs.

Mike: Ah, of course. What’s a typical managing director salary?

Banker: $300,000 to 400,000.

Mike: And the bonus on top of that?

Banker: It varies a great deal.

Mike: Throw a range at me.

Banker: Anywhere from $100,000 to $10 million.

Mike: !!!

Banker: There are MD’s in technology and HR who won’t ever get a large bonus. Then there are the “rainmakers” in investment banking who will generate hundreds of millions in revenue for the firm with just a few large deals. They are the highest paid people at banks, outside of the senior executives. Some of the “best” (or luckiest) traders used to make that much, too, but that’s much less common these days.

Mike: So we’re talking about a lot of money here. This means early retirement?

Banker: Depends what kind of lifestyle you have to maintain.

Mike: So what’s that for you?

Banker: Lets take a look at Mint. The goal for me is to be able to be happy with a modest enough lifestyle that when it’s time for me to have kids, I won’t be a slave to the salary.

I spent about $85,000 last year, according to Mint, which doesn’t count charitable contributions.

• ~$31,000 is rent

• $15,000 food and dining

• $10,000 travel

• ~$8,000 bills/utilities

• ~$7,000 shopping (mostly gifts)

• ~$6,500 unallocated cash

Mike: And that cash could also be for anything like food or taxi rides?

Banker: Correct.

Mike: What did you put into savings and retirement last year?

Banker: Good question! I max out my 401(k) every year. Then another $65,000 on top of that — so around $82,000.

Mike: So, that was $17,000 last year in a 401(k). And then $65,000 in a savings account? Or invested in mutual funds?

Banker: Right, the $17,000 goes into a 401(k) with investment choices limited by my employer. That account has about $150,000 in it now. Then the $65,000 goes into a brokerage account. Which is mostly invested into a dozen individual stocks and mutual funds. That’s about another $350,000 total.

Mike: Is this an account you’ve had since you were a kid? Saving money and sewing buttons?

Banker: Ha. I mean, yes, but the vast majority is what I’ve saved since college. I think I had maybe $10,000 when I left college, or something like that. I’ve also invested in a small business started by some friends, which is my largest and riskiest investment.

Mike: Oh, investing in your friends is always a big risk. Putting relationships on the line!

Banker: That is true. But, for me, as long as our incentives are aligned and it’s not so much that if I lose it all, it will ruin my life, it’s ok.

Mike: Is there anything in particular you’re saving for? Do you want you buy an apartment in the city?

Banker: God no. I mean, I would if I thought it was a good investment. But housing in New York is crazy expensive, even for someone who makes a lot of money. I don’t feel secure enough in my income to be able to commit to a mortgage payment. I think a lot of people (even rich people) who lived through the housing bust feel that way. If I moved away from New York to someplace with fewer good rental options and cheaper overall housing, I would buy a place. Or if I found a place where I knew I wanted to be for the next 10 to 20 years (and could afford it even with much less income).

Mike: I’m sure that will also depend on what kind of family you’d like to have. Are you dating?

Banker: Right! I am dating someone. It’s serious. We live together with two cats. So, yes, buying a place would be a longer discussion, but my girlfriend and I have talked about my views on buying a house. And she agrees that it doesn’t make sense in New York. If we moved away, who knows.

Mike: Does your girlfriend earn as much as you do?

Banker: Nope. She earns a more “normal” living — way above the median U.S. income for a single white woman working full-time (which was about $40,000 in 2011), but normal by New York standards.

Mike: How do you navigate money in your household? Do you mostly pay for things?

Banker: I pay more — we split most of the expenses 60/40.

Mike: So when you say you spent $31,000 on rent, that was just your share?

Banker: Yes.

Mike: You must have a nice place!

Banker: Well, now I’m checking again, and that included a broker’s fee. On a straight up rent basis my share would be around $20,000 a year. But yes, we do have a nice place in a nice neighborhood, which is a great luxury. But I pay significantly less rent than most of my work peers.

Mike: What are your work hours like?

Banker: Twelve hours most days — I get in around 8:30 a.m. and am checking my Blackberry until I go to sleep.

Mike: Do you work weekends?

Banker: I usually end up working at least a couple of weekend days per month. The first three years in the job are the most brutal. That was 6:30 a.m. to 10–11 p.m. Monday through Thursday and working pretty much every weekend. I still end up pulling a couple of all-nighters every year.

Mike: What’s your social life like?

Banker: I think its pretty normal — drinks with work people some Thursday or Friday nights, and I go out with non-work friends on the weekends, and I have normal hobbies. It’s not like I’m sitting in a dark room counting my money like Scrooge McDuck.

Mike: You do consider yourself “rich” though, yes? Especially if you continue on and become a managing director.

Banker: Yes, I do consider myself rich, even if I don’t make it to managing director. Mostly that’s not about my income, but about the nest egg I’ve been able to save. So, some stats:

• Only 5% of white males age 25–29 earned more than $100,000 in 2011

• The median net worth of a head of household under 35 years old is $12,000

Mike: Well, I’m glad you have some perspective.

Banker: There was a great article I read: “Straight White Male: The Lowest Difficulty Setting There Is”

I was very lucky growing up — financially and emotionally stable parents. Being lucky can’t be the answer though. It’s not helpful. That’s why it’s sooooo important to have as even a playing field as is possible.

Mike: And how do you think we can even the playing field?

Banker: Good public schools help. If people believe the system is fair, and you give them the tools and opportunity to learn a skill, the rest will usually work itself out. But having a fair system is crucial. There’s a book called Animal Spirits by George Akerlof and Robert Shiller that provides a great overview of the financial crisis and how it created more unfairness in our economic system.

Mike: Does this mean you’re happy to pay your taxes?

Banker: Well, no. I don’t think anyone is happy to pay their taxes. But yes, I do believe in a progressive wealth redistribution system. I think consumption taxes would work better than income taxes, and I think we need an aggressive carbon tax. So: I’m not a Republican!

Mike: So, when you first got in touch with me, you told me you were going to inherit some money.

Banker: Right, so to me, inheriting money is the most unfair way to “win” the little game we call capitalism. The idea that money (and therefore power) can be freely given to someone undeserving is the opposite of fair. I mean, winning the lottery is so much more fair, because at least that’s random. And the best way to avoid an aristocratic layer of society is to have a high (close to 100%) inheritance tax. So you can imagine my dismay when my parents recently told me that I’m probably going to inherit some money. I’m grateful that they didn’t ever tell me when I was younger. Anyway, more rich people problems, right?

Mike: It seems like your parents did a good job of trying to let you see the value of hard work, and provide you with some perspective. Can you say how much you’ll be inheriting?

Banker: I don’t know!

Mike: But you think it’s quite a bit.

Banker: Not enough to retire on. But probably a couple of years of living expenses, if I ever need it. It’s amazing what kind of breathing room having a cushion like that can bring. Putting aside the issue of inheritance — just knowing that you’ll be ok for a year or two if you lose a job…now that I have that peace of mind, I can’t imagine living paycheck to paycheck. And I know that the vast majority of people who do get laid off every year don’t have that flexibility.

Mike: That’s one less thing to worry about, for sure.

Banker: When it comes to money, I have less to worry about than 99% of the people out there, but that doesn’t mean I don’t worry about the future. If I didn’t have anything to worry about, would I work 12 hour days? Probably not. Being so close to the financial markets when everything was going to hell, I don’t think I’ll ever feel truly “safe.”

Mike: The Queen of Versailles.

Banker: Right. Another reason to live more modestly than you need to!

Mike: Is there anything we haven’t talked about that you think we should cover?

Banker: Probably. I could spend another two and half hours talking about investing.

Mike: Haha. Let’s save that conversation for another time.

Previously: A Friendly Chat With a Rich Person (Household Income: $360,000)

Questions? Interested in talking to us about your money? Send an email.

Support The Billfold

The Billfold continues to exist thanks to support from our readers. Help us continue to do our work by making a monthly pledge on Patreon or a one-time-only contribution through PayPal.

Comments