My Sister’s (Book)Keeper: I Don’t Think This Is Working…

Things get tense when talking dollars and cents.

This is the fourth in a series of articles about sisters and budgeting (read the first, second, and third posts). Genie, a frugal 29-year-old, attempts to mentor her sister Kate, a spendthrift 31-year-old, in the messy and confusing world of personal finance. How do you help your family manage their finances without going insane or completely destroying your relationship? We’ll find out.

Kate

Look at me, Mom! I’m budgeting!

My accounts were linked to my budgeting software, and I had downloaded the companion app for my phone. Now that the plan was in place, I would magically become a frugal, responsible adult who handled her expenses and planned for the future. That’s how I felt at the end of my YNAB set-up session with Genie. I was ready to overcome all of my financial shortcomings. Oh, if it only it were that easy.

Genie

We decided to have check-ins at least once a week to see how things were going. We would schedule time to get on Skype and talk about any problems Kate was running into. To my dismay, though, the first few times we checked in, we spent most of the time just entering in the transactions Kate hadn’t been tracking during the week, and then realizing she was already overspent in some places. We had to start covering her overspending with money we’d been trying to set aside for things like vacations or an emergency fund, and before we knew it we’d be back to square one.

Kate

Genie is the Queen of Self-Discipline. I am not — I’m not even a princess. Honestly, when it comes to self-discipline, I’m not even invited to court. I had the tools to make my budget work, but I still had all of my bad habits when it came to managing money. I bought things impulsively and looked at my bank account balance to signal whether or not I had money to spend. (This is when Genie would remind me that the whole point of budget categories and building emergency funds is NOT looking at your bank balance. I would usually roll my eyes in response.) Budgets are all well and good, but I was not changing my habits as quickly as Genie seemed to be demanding.

Genie

Well, I wouldn’t say I was demanding. But I did want to see her making an effort to change her habits, and from my perspective (across the country and never seeing her in person), she wasn’t making that effort.

Frustrations started to flare. I would get annoyed with Kate’s spending and refusal to check her budget and I’d start lecturing. Kate would get angry that her little sister was on a high horse telling her how to live her life. It was not always (ever?) pretty. Sometimes Kate would be really difficult when it came to scheduling our next check-in, and I knew it was because she was feeling anxious about her financial situation. But I still got angry, and was mean to her when she bailed on a session. I wish I could say I was patient, but I wasn’t.

When we did check in, we started to notice one item that was really tripping Kate up.

Kate

I didn’t want to disappoint Genie (or be in debt). The first place for major improvements: credit cards. The balance was never going to get significantly smaller if I didn’t do two things:

- Stop spending. (This seems obvious, I know). If I had to use the credit card for whatever reason (taking advantage of double points at certain stores or needing something a few days before payday), I had to be sure the cost could be paid off immediately. It was still coming out my current budget, and my current budget was coming from all the dollars I had. Period.

- Account for interest. Even if I stopped using my cards completely, interest payments would make it difficult to make a dent in my debt. I had to account for my minimum payment plus any interest that had accrued during the pay period. This was the only way to make my balance get smaller in any significant way.

Logically, I understood this credit card plan. It made sense on paper. But in reality, this was so hard. If I kept credit card interest in mind, it was adding a new expense into my monthly budget. Where was that money going to come from? I started to worry that getting debt under control would require eating nothing but peanut butter and crackers. Moments like this are when I let panic take over — and I’m not particularly enjoyable when I’m panicking.

Genie

It also didn’t help that logistically, the YNAB app was really confusing her in relation to credit cards. I tried to remind her that YNAB had whole classes online she could watch explaining how to input and track these things, but she wasn’t interested. So I explained it myself.

As we know, YNAB wants your credit card spending to come out of your budget. You use your credit card at a restaurant, and the amount is deducted from your “eating out” budget, just like any other spending. However, you also have to pay off these cards at some point, and they don’t want you to forget that. So when you spend on a credit card, that amount also shows up at the top of your budget in your available money for credit card payments. This is so you can easily see how much you’ve spent on that card and need to pay off this month.

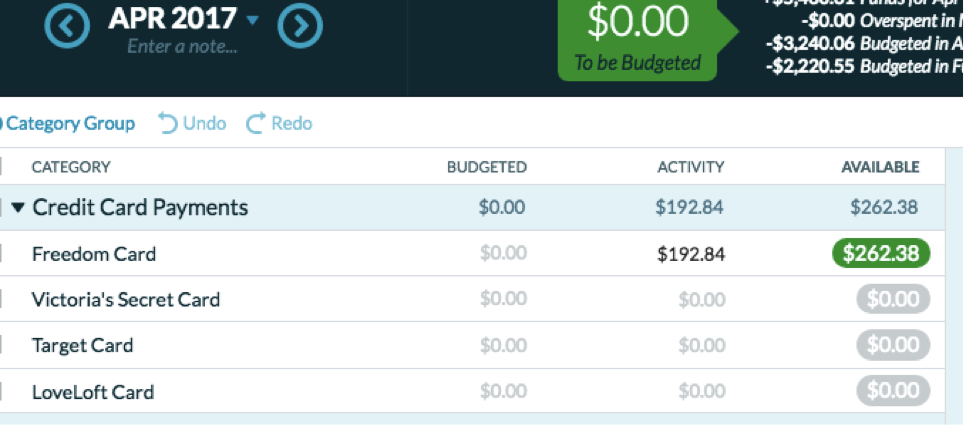

Let’s look at an example. This is a screenshot of my current credit card categories (don’t judge my choice of store credit cards).

I’ve used my main credit card to spend in several budget categories, and each of those amounts is both deducted from that spending category, and added to this available credit card payment category.

So if I spend $50 at Safeway on my Freedom card, that $50 is subtracted from my groceries budget. That $50 simultaneously gets added to the green amount in my available column for that card — that money was budgeted for, has been spent on the card, and is available to be paid off at any time.

So as long as I’m staying within all my budgets, at any time of the month I can glance at this green available number for a credit card and say, “I need to pay off $262.38 on this card and I have all the money to do that.”

If money was spent on a credit card that you didn’t budget for, the amounts would still be reflected here but the available money would be yellow instead of green, because you haven’t actually funded all those categories you spent from.

Now, with Kate’s cards, we were also dealing with debt. So that means in the “budgeted” area, she needed to be budgeting for the minimum payments plus any extra she was able to put toward the debt. It got a little more complicated with all these moving pieces, and it took us a few instances of scrolling through transactions and manually adding them up to figure out where the balances were coming from. But eventually, we were on the same page — if everything was budgeted properly, all she had to do was pay off the amount in green for each card at least once a month.

Kate

I can admit that I was being a bit of pouty brat in refusing to read or watch the online resources. But I can also say that credit card tracking on YNAB is not always intuitive. Even the categories confused me at first: budgeted, activity, available.

But, if I’m being honest, I would sometimes “budget” an amount to pay on the card, then buy something new and try to say my budgeted money was for that and not for paying off the debt. I was fooling myself for a long time.

(I should mention here that everyone needs to find what works for them. I am sticking with YNAB mostly because I have finally gotten the hang of it, plus Genie is a self-proclaimed expert who can help me when anything stumps me.)

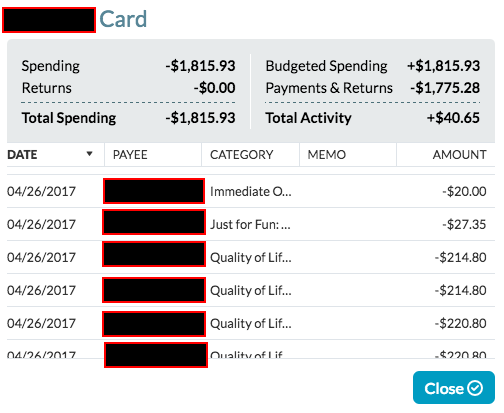

Ultimately, what worked best for me was just not looking at the column labeled ‘Activity’. It only showed transactions for the current month, and was harder for me to follow.

If I wanted to see transactions for a particular card, I would just select that card under accounts. I could see all the transactions and it wasn’t as confusing.

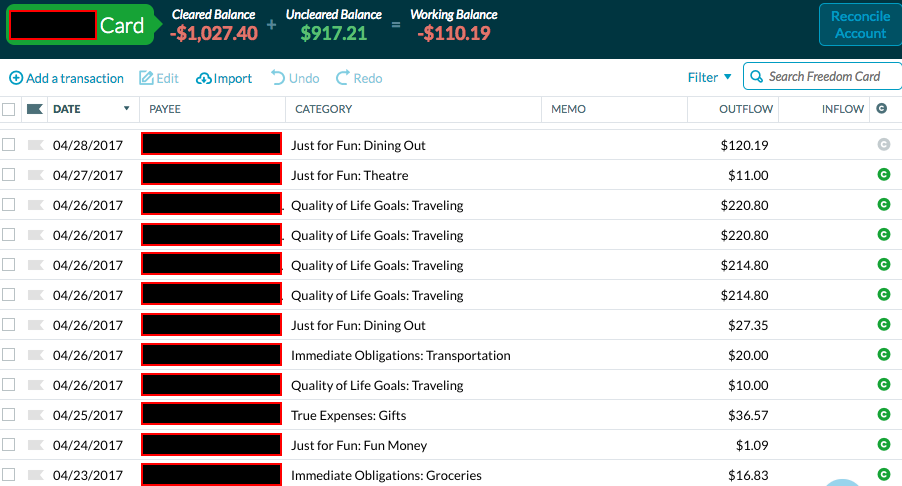

In my budget, the best thing to do was look at the (hopefully) green ‘Available’ column to dictate how much I should pay on the card. It sounds easy but it took me months (and a number of tense phone conversations with Genie) to get the hang of it.

Genie

I didn’t know how to help her establish good habits. She’s an adult, I can’t make decisions for her. I tried to emphasize how great it had been for me when I eliminated my credit card debt. I tried to show her things I’d been able to pay for because I’d planned ahead. But I was starting to feel like I came across as a know-it-all bragging about how good I was at this instead of being helpful.

I also knew that my pushy, tough-love attitude was making her uncomfortable. She would push out our check-ins, bail at the last minute, and then when we were finally talking together she’d get all cagey about what she’d spent her money on. But whatever else I couldn’t control, I was adamant about this: we are not hiding from our financial decisions. We may not be proud of them, but not facing them helps no one. I promised her I wasn’t going to judge, but I also wasn’t going anywhere until we both took a look.

Kate

Why is there such a stigma about discussing money? I wanted to go up to my friends and say, “Hey, how was your week? I’m in debt and I’m scared I’ll never get out.” But most people would consider that uncool, so we all just pretend that everything is fine.

It was really hard for me to be completely honest about what I was choosing to spend my extra money on. And I really hate admitting I’m wrong. Genie knew what I was making at this point, but if I slipped up within one of my budget categories, I just avoided her. This put a strain on our relationship and it certainly wasn’t helping my financial situation. I found it really hard to even explain how overwhelmed I was. Why wasn’t this easier for me? If Genie could do it (and had been doing so for a while), why couldn’t I? Was I some sort of adult failure? I was getting so frustrated that I considered throwing in the towel and accepting that I would be poor forever.

Coming up next in My Sister’s (Book)Keeper: How to establish a financial routine? Genie talks about her own financial system for meticulously tracking her funds and doesn’t understand Kate’s challenge to develop her own habits.

Genie Leslie is a writer and actor living in Seattle.

Kate Leslie is a theatre educator and director living in Chicago.

In between budgeting sessions, they host the podcast The Musical Version with their younger sister, who has not sought out any financial advice at this time.

Support The Billfold

The Billfold continues to exist thanks to support from our readers. Help us continue to do our work by making a monthly pledge on Patreon or a one-time-only contribution through PayPal.

Comments