My Sister’s (Book)Keeper: Forming Routines and Establishing Habits

Genie’s way or the highway?

This is the fifth in a series of articles about sisters and budgeting (read the first, second, third, and fourth). Genie, a frugal 29-year-old, attempts to mentor her sister Kate, a spendthrift 31-year-old, in the messy and confusing world of personal finance. How do you help your family manage their finances without going insane or completely destroying your relationship? We’ll find out.

Genie

We’ve talked a lot about how Kate needs a system, how I have a system, and how I wish she could just follow mine and do everything like I do. So let’s talk about what my system actually is.

My system is the standard YNAB system (I’m pretty sure). When I get a paycheck, I make sure to budget out every single dollar somewhere. If I’ve got extra after all my categories are covered, the extra goes to savings or to the next month. For the first part of the month my categories don’t usually change much. It’s in the second half, as I’ve started to spend more, that I start adjusting amounts. But I’m never pulling from my emergency fund or, if i I can help it, money budgeted in future months. If I overspent on fun money, I have to pull the extra from dining out or groceries—some other category in this month.

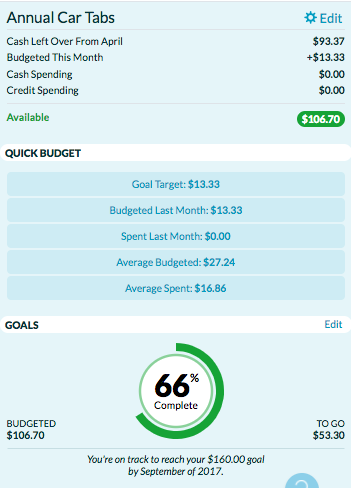

I’m also following the YNAB rule of planning for annual expenses. Right now in my budget, I have a category for renewing my car’s license plate in September. It’s expensive here in Seattle and it always sneaks up on me. So last September I started a category for Annual Car Tabs and set a goal of saving $160 in a year, by September 2017. YNAB told me I needed to put about $13 aside each month to reach this goal, so that’s what I’ve been doing. That money is in my checking account but I never think about it, because it’s spoken for in my budget and it’s in a category that I don’t touch.

Kate

Planning for annual expenses? Ugh. Genie tried, she REALLY tried, to get me into this habit right away when I started budgeting. Something she had to accept (or pretend to accept) was that it just wasn’t going to happen for a while. Sure, I knew when my car tag would expire or that I might have to buy a plane ticket in the next few months, but there just wasn’t any extra money to go around. Also, my brain is not wired the same way Genie’s is — planning for one purchase (like my car tag) a year in advance wasn’t something I was interested in.*

My solution was in the form of two budget categories: Emergency Fund and Stuff I Forgot to Budget For. Genie cannot stand my “Stuff I Forgot” category. But it really comes in handy. It’s just a small amount of money I set aside every month for unexpected or odd spending. Genie does have her own Emergency Fund, but I’m pretty sure that what I deem worthy of an emergency does not pass Genie’s litmus test. But when I was first starting, this really worked for me. I wasn’t able to build these categories up very much because almost every month I was dipping into them for one thing or another. BUT I was almost always able to cover my expenses with the money I had in the bank, and that was my first goal.

*I would like to add that this was my thinking at first, and I have gotten over this… or I’m working on it.

Genie

A couple of notes: I’m currently budgeted 25 days ahead, so almost a month. That means that as I’m writing this, on May 28, I’ve already budgeted for June’s rent, student loans, and most of the bills. When I get my paycheck on May 31, I’ll budget for June’s fun categories — eating out, fun money, my haircut — and then the rest of the money will to go to July’s rent and student loans.

Building up this cushion is great, but it’s also not super easy to do. I mean, you need extra money to make it happen — I was able to make a lot of progress on it because of an unexpected $3,000 I received last year. So it can be a frustrating goal when your progress is slow. But it’s worth it. This cushion has been huge for my mental state. When I first moved to Seattle, I was a freelancer with no idea where my next check was going to come from and I thought (stressed) about money all the time. Now that I have this buffer, I have peace of mind. When work is slow and I’m making less, I know I’m okay. If I lose my job tomorrow, I know I wouldn’t be in an immediate crisis. This is why I love YNAB so much.

Kate

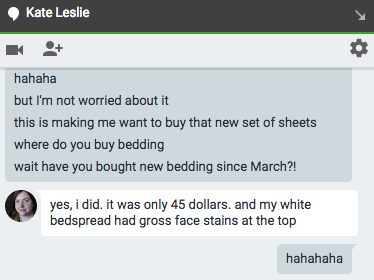

I think Genie’s ability to build up this cushion was 90% pure determination and 10% YNAB. Genie has also been working a job for the past two years where her paycheck might change from month to month. When her check was a little bit larger than normal, it was easier for her to put away money for her cushion. Plus, Genie is frugal, and I am easily tempted to make purchases. I’m impulsive. Sure, I might not need that new bedspread RIGHT now, but it’s on sale and it’s pretty and I have the money to buy it. If this were Genie, building her cushion fund would win out over new bed linens. But me? It’s pretty AND my favorite color AND it’s on sale.

You probably won’t be surprised to learn that I’ve been sleeping under a new, mint green comforter, and I love it. (Genie was actually surprised by this and did not approve — at first.)

Genie

It’s true. I’ve been meaning to buy a new set of sheets for my bed for four years, but that money always ends up going somewhere else. I really need a new set of sheets. Buuuuuuuut I could age my money a couple of more days!**

The other important element of my system is tracking. I’m a Type A, fastidious tracker. I can’t help it. When I got my first bank account, I wrote down every debit card purchase in the little bankbook that they gave me. Now I do it in my YNAB app on my phone. When I finish a meal out, I make my boyfriend or my friends wait for me to enter in my transaction before we leave the table. If I can’t make people wait, I stuff the receipt in my pocket so I can enter that amount just as soon as humanly possible.

I want to know, in any given moment, how much is available for me in my categories. This is why I never liked systems like Mint. I don’t want to wait two days for my transactions to clear the bank, especially in situations like vacation or weekend days when you might be spending money in a few places in one day. I love that YNAB connects to your bank account, so that if I do forget to enter something, there’s a backup for that transaction. But I can continue to enter my transactions manually and then they’ll just match up with the imported bank transaction without any extra effort from me. It’s the best of both worlds for me.

**It should be noted that I did buy two new sets of sheets after writing this draft. I spent $80 at Target, taking advantage of 5% savings and free shipping by using my Target credit card, plus 30% savings for Memorial Day sales. I pulled the money from my traveling budget category, which will be replenished out of my next paycheck. Turns out, Kate’s impulsivity may be rubbing off on me a tiny bit, and that’s okay.

Kate

Even though I had trouble consistently inputting my spending, YNAB did make it easier for me. For example:

Let’s say I frequent a particular Dunkin’ Donuts at least 3 or 4 days a week (you may recall, I have an iced mocha addiction). On the days that I think to input my purchase as I am waiting for my caffeine treat, my YNAB app remembers the location of this Dunkin’ Donuts. Once I fill in the purchase amount, the app suggests that I am at my favorite breakfast place and categorizes the expense from my Dining Out budget — a very helpful feature that saves time. Then I am able to see in real time what I have left in my Dining Out category — before I consider buying another iced mocha that afternoon. This has been helpful for me.

Even though I struggled for quite a while (and still do), I have made progress on my financial goals thanks to YNAB.

We’ve discussed before that one of my challenges was conquering (still trying to conquer, more accurately) credit card debt. The key to really tackling this debt was budgeting for interest as it accrues. Once I input these charges into YNAB, the software would remember how these categories should be budgeted. This took some of the guess work out of budgeting — all I had to do was ensure that there was money to cover my Interest Payments category. It didn’t happen right away, but after some time, those credit card balances started to go down.

At the end of the day, I don’t budget exactly like Genie does. I still may go a few days without inputting all my transactions. I sometimes budget after the fact. This drives Genie bananas, but as long as I haven’t done anything too crazy, this works for me. And forming my own habits that I can stick to is a definite win.

Coming up next in My Sister’s (Book)Keeper: We’re wrapping this up! We’ll talk about where we are now in comparison to where we started, and what our goals for the future are.

Genie Leslie is a writer and actor living in Seattle.

Kate Leslie is a theatre educator and director living in Chicago.

In between budgeting sessions, they host the podcast The Musical Version with their younger sister, who has not sought out any financial advice at this time.

Support The Billfold

The Billfold continues to exist thanks to support from our readers. Help us continue to do our work by making a monthly pledge on Patreon or a one-time-only contribution through PayPal.

Comments