When You’re Not Saving Enough to Retire at 65

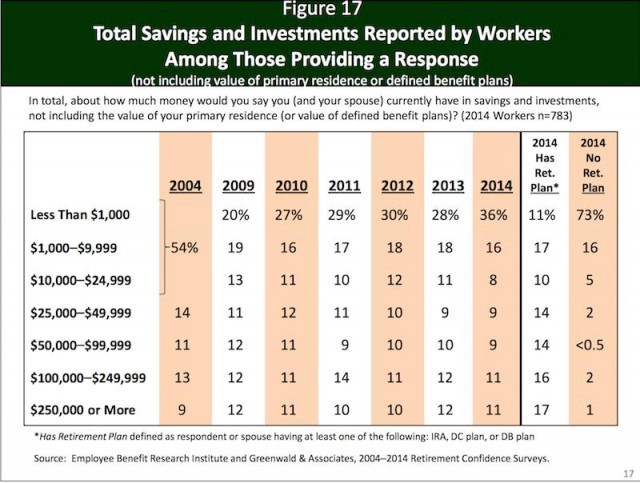

The Employee Benefit Research Institute recently conducted a 20-minute phone survey of 1,000 workers and 501 retirees ages 25 and older to discuss “retirement, their preparations for retirement, their confidence with regard to various aspects of retirement, and related issues.” The full report is here, but this chart with total savings and investments will probably interest you since more than a third of respondents said they had less than $1,000 in savings:

So if you’ve got a little hitch in your git-along (as my family down South would say) when it comes to saving for retirement, you are not alone. What is your game plan?

The most obvious answer, is you will work longer — as least until you are 70, says the Wall Street Journal. That’s because the longer you wait to retire and hold off on collecting Social Security payments, the more you can collect later:

Let’s say your full Social Security retirement age is 66, at which point you could get $1,400 a month, equal to $16,800 a year. This is roughly the average amount that Social Security recipients are entitled to.

If you claim at 62, you would take a 25% hit, leaving you with $1,050 a month, or $12,600 a year. By contrast, if you delayed benefits from 66 to 70, you would get 32% more. That would mean $1,848 a month, equal to $22,176 a year. This doesn’t reflect any increases because of inflation.

True, $22,176 at age 70 won’t pay for a lavish retirement. But unless you have a lot of other income, you shouldn’t have to pay taxes on your Social Security benefit. Indeed, Social Security is perhaps the best income stream available to retirees. It’s indexed to inflation, backed by the federal government, at least partially tax-free, and you know you’ll get it for as long as you live. Moreover, your spouse may receive your benefit as a survivor benefit, assuming you die first.

If you’re lucky and willing and able, you might be able to continue to find work later in life if you don’t have enough money saved and still want to live comfortably and be the kind of Golden Person who can plan and take occasional trips (see the story of 77-year-old Tom Palome in a previous post I wrote about the retirement crisis).

But life doesn’t always work out the way you would like it to. Many workers are forced to retire early because they’ve become “redundant.” My father, who set some money aside for retirement but not nearly enough, was forced to retire early after injuring himself at work and spent the majority of his time afterward in a legal battle for disability payments (which he eventually won). He’s now collecting Social Security.

And what happens when he’s short on cash?

Well, he’s got me.

Support The Billfold

The Billfold continues to exist thanks to support from our readers. Help us continue to do our work by making a monthly pledge on Patreon or a one-time-only contribution through PayPal.

Comments