My Sister’s (Book)Keeper: Setting Up and Getting Started

Time to put the plan into action.

This is the third in a series of articles about sisters and budgeting (read the first and second). Genie, a frugal 29-year-old, attempts to mentor her sister Kate, a spendthrift 31-year-old, in the messy and confusing world of personal finance. How do you help your family manage their finances without going insane or completely destroying your relationship? We’ll find out.

Genie

After having gone over the rules and mindset changes, it was time to get into the details. We slowly went through the process of connecting Kate’s accounts. In YNAB, most accounts will be on-budget, meaning any money you spend will need to come out of the budget you have right now. These would be checking accounts, savings accounts, credit card accounts. But long-term debt accounts, like student loans, should be off-budget (these are now called “tracking” accounts). You’ll still have a category and need to budget for these payments, but any extra money spent, like accrued interest, does not have to come out of your current budget — because YNAB’s creators understand that student loan interest is the worst, and we’re all doing the best we can.

Now with the connected accounts, it was time to input her income and start to budget it out. We started on a payday to make this process easier — she had just gotten her money without a chance to spend it.

Kate

For me, using a budgeting system that could connect to my different accounts was important. This lessened the burden of having to input every single transaction immediately. Once my accounts were connected, it was time to start officially integrating YNAB into my monthly financial plan.

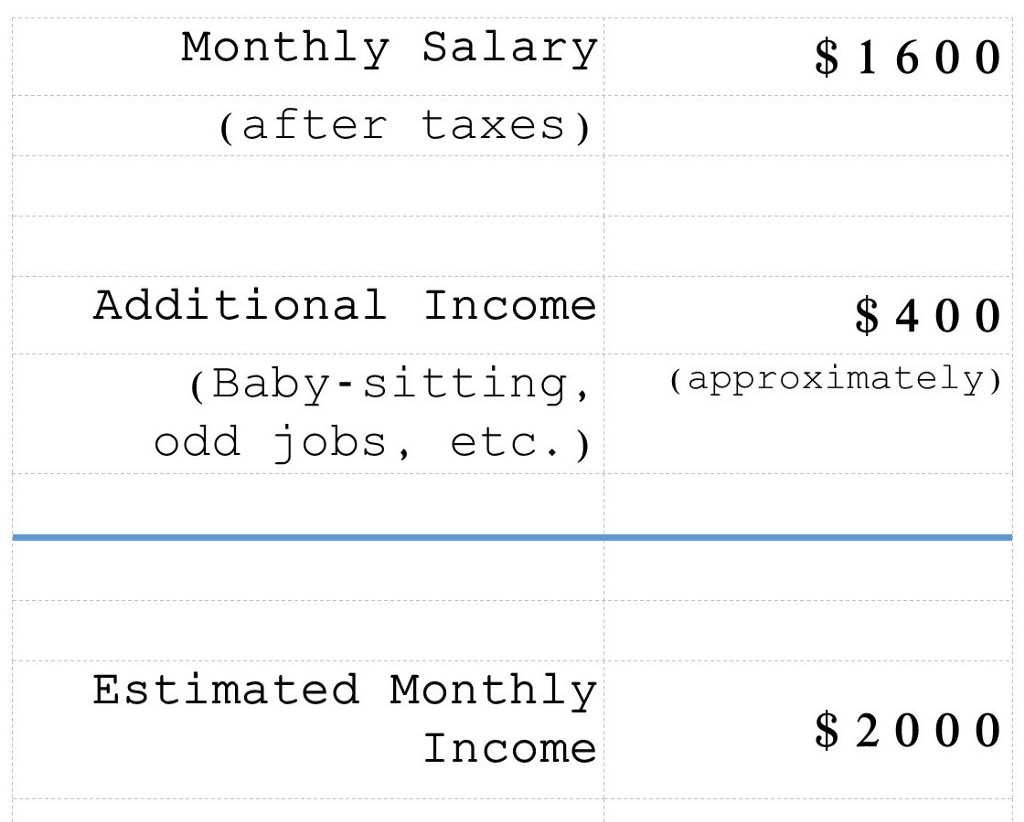

Step one: How much money am I making each month? I had a few side jobs, so I needed to estimate what portion of my income was coming from extra work.

The numbers below represent approximately what I was making when Genie and I started this project in April 2015.

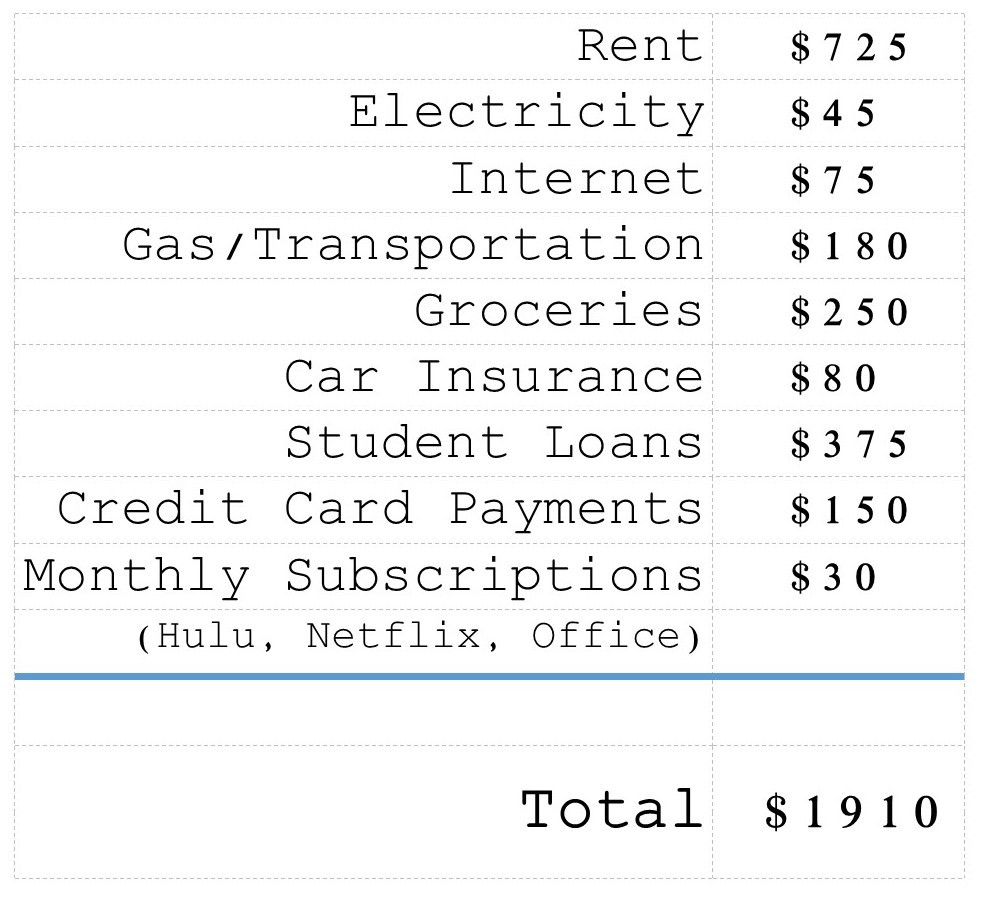

So, I usually had $2000 to work with each month. This had to cover all my bills, loan payments, groceries, and anything fun. Ideally, I would also not add any more debt to my credit cards. Genie thought it would be a good idea to estimate most of my monthly expenses.

As you can tell, my budget was fairly tight.

Genie

This is where helping Kate started to really throw me for a loop. Honestly, I had been harboring a little frustration with her — why can’t she just get it together and be more disciplined with her money? — and seeing the actual numbers she was working with was eye-opening. She was making a good bit less than me. She was living on her own, not sharing rent or bills with anyone else. We hadn’t even included dining out or other fun money and she was already exceeding her monthly salary! Of course she had places she could improve, but she wasn’t just lazily throwing money out the window on anything and everything. She was trying and I needed to acknowledge that.

Kate

I remember when Genie finally saw the whole picture. She was shocked to see how much money I made (or rather how little) and how much time outside of work was spent earning extra income. This didn’t mean that she started going easier on me in terms of my financial transformation, BUT she did gain a whole new understanding of my stress and anxiety around money (which was the whole reason for starting this project!).

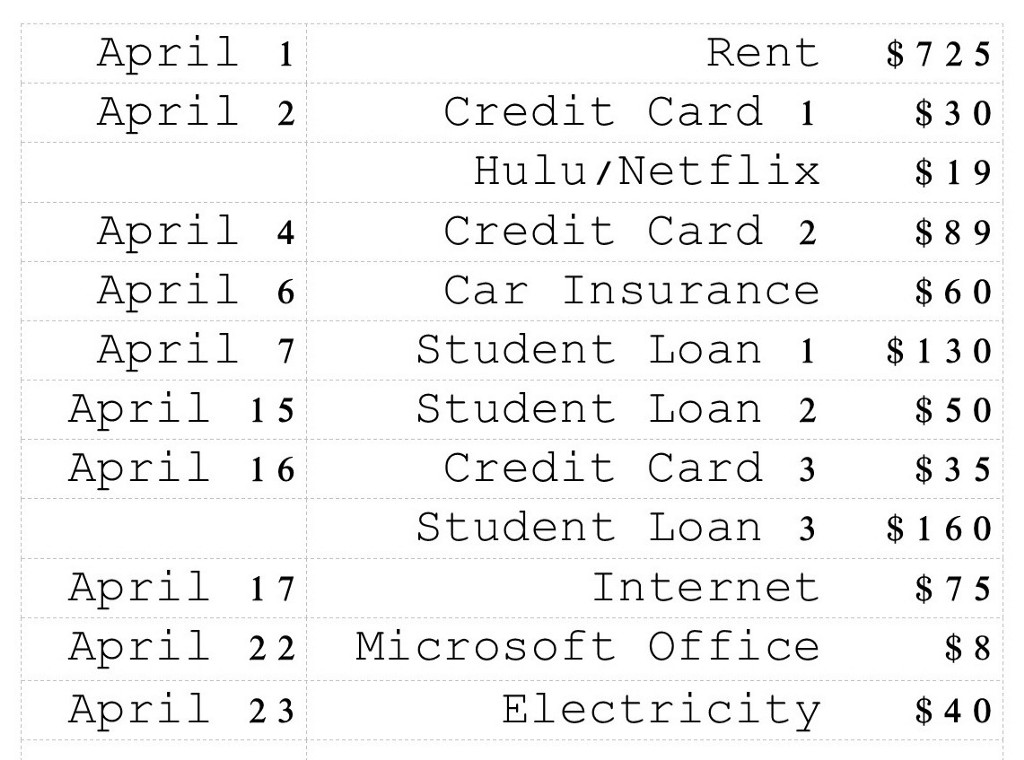

One of the best things she taught me was how to really attack my bills in a way that suited the cycle of two paychecks a month. First, I had to know when bills were due. I had occasionally gotten myself in trouble by thinking I had paid a bill when I hadn’t, and by the time I realized the mistake, I had already spent the money. This is what happens when you spend money based on your checking account balance.

Getting paid twice a month made budgeting more difficult. With $1600 for the whole month’s salary, that meant one paycheck was just $800. Genie insisted that I make a list based on due dates. Below is a list of my bills in April 2015.

Genie

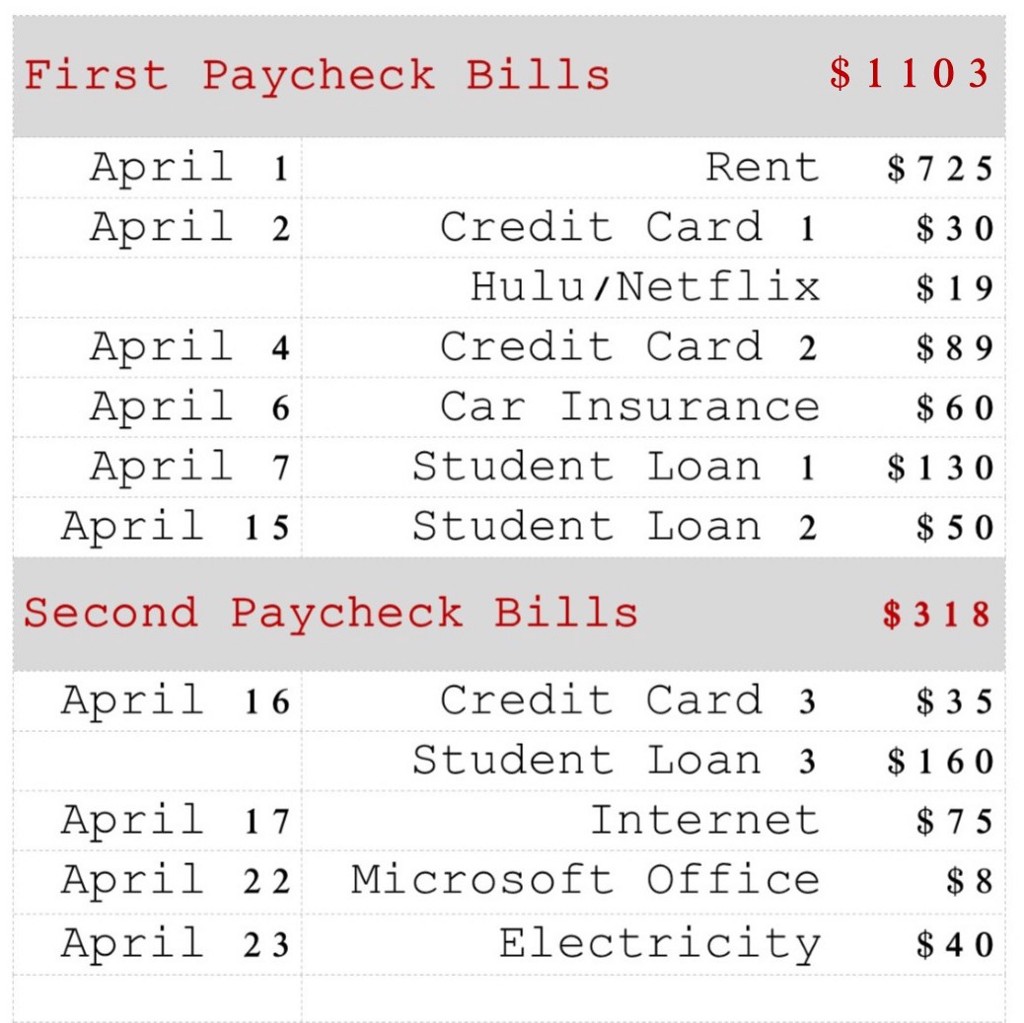

Now that we had the date list, we needed to divide it up by paycheck. As a person who receives a bi-monthly paycheck myself (yep, I’m a writer), I had done this with every new job and/or new apartment and set of bills.

So, this was the new bills list, now also divided by paycheck.

Right away we’ve got a problem. One paycheck was roughly $800, but the bills in her first paycheck list were more than that. Baby-sitting money and odd jobs could potentially add to that income, but those were not on a regular or reliable schedule. No wonder she’d been relying on credit cards.

But this was also a chance for the YNAB system to really shine. What we needed to start doing was taking money from that second paycheck of the month, and setting it aside for the early bills of the next month. This was where the self-discipline and regular budget checking would come into play. Kate needed to be able to set that money aside for the next month and not touch it for anything else.

Kate

Of course I had realized that the majority of my bills were due at the beginning of the month. I was already in the habit of paying all of my student loans in the middle of the month, even though two of these loan payments were two to three weeks early. But setting money aside for specific expenses (as Genie was suggesting) was not how I had approached my budget in the past.

Genie

Now that we had our lists and our dates to follow, we budgeted out her actual money. And then she caused me great anxiety by trying to budget more.

Remember, YNAB is all about budgeting the dollars you have right now. So if you are paying your car insurance bill out of your second paycheck, you aren’t going to fill in that budget category until the second paycheck has come in. But Kate could very easily forget to pay the bill without a reminder. So after we budgeted out all the dollars from her first check, she wanted to go ahead and fill in the car insurance category as her reminder.

Two Sisters Who Don’t Think Alike: A Short Play

Genie: Wait, what are you doing?

Kate: I’m just going to put this here so I know to pay it when the time comes.

Genie: But…but…you don’t have that money now! See, now you are over-budgeted by $80.

Kate: But if I don’t put it here, I might forget.

Genie: But…see? The ugly red -$80 at the top? Doesn’t that bother you?!?!

Kate: Nope.

Now, the truth is, this wasn’t that big of a deal, especially for starting out. If she already had it budgeted, when she input the income from her second check, it would adjust for that -$80. She wouldn’t end up budgeting it twice or anything. So if that’s what she needed to do at this point in the game, that should’ve been fine. But my rigid brain just reeeeeeeeeally wanted to her to follow the system’s rules and not budget out ahead.

But we moved on, and I let her leave her ugly red -$80. It wasn’t worth a fight, and we had more to do.

We were going to have to acknowledge her credit cards. She was in debt and needed to get it under control. There were two actions that needed to be put in place: 1) Not creating more debt. No more money spent on credit cards that you can’t pay for out of this month’s budget. Anything new you spend on a credit card gets paid off in full this month. 2) Starting to pay MORE than what was spent on a card this month, in order to bring the debt down. This would require planning and saving for those extra payments. More on this later.

Kate

This budget business was getting real. I had a system for making sure bills were paid on time and not forgotten about. No need to waste money on late fees when they could be avoided. And I was determined to stick to the new credit rule: no more credit card debt! I had to really dedicate myself to paying down those debts every month while keeping everything else in check. I was going to need to channel some of Genie’s intense self-discipline if this was going to work.

Coming up next in My Sister’s (Book)Keeper: With the budget set up, it’s time to stick to it! We start working with weekly check-ins to deal with tracking expenses, covering over-spending if/when it happens, and dealing with credit cards.

Genie Leslie is a writer and actor living in Seattle.

Kate Leslie is a theatre educator and director living in Chicago.

In between budgeting sessions, they host the podcast The Musical Version with their younger sister, who has not sought out any financial advice at this time.

Support The Billfold

The Billfold continues to exist thanks to support from our readers. Help us continue to do our work by making a monthly pledge on Patreon or a one-time-only contribution through PayPal.

Comments